All conferences and presentations are in English. Translation (english to spanish) will be provided for Paul Embrechts´s Opening Plenary Session and Spanish to English translation will be provided for Clemente Cabello´s Plenary Session on Thursday.

DOWNLOAD PROGRAM HEREDOWNLOAD WORSHOPS BRIEFING AND INFORMATION HEREPARTICIPANT´S LIST

ASTIN Commitee meeting

AFIR Commitee meeting

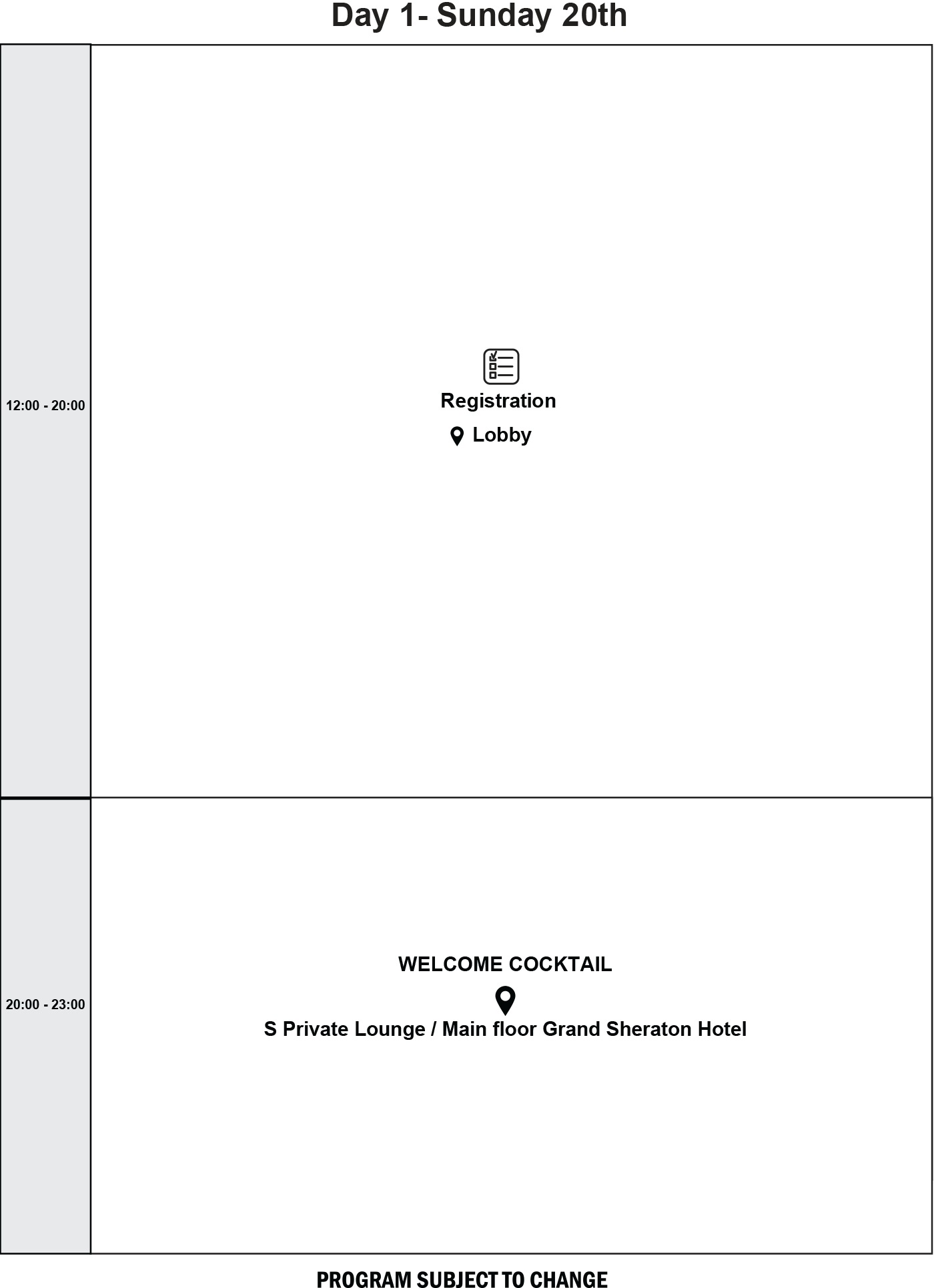

Registration

Welcome Cocktail

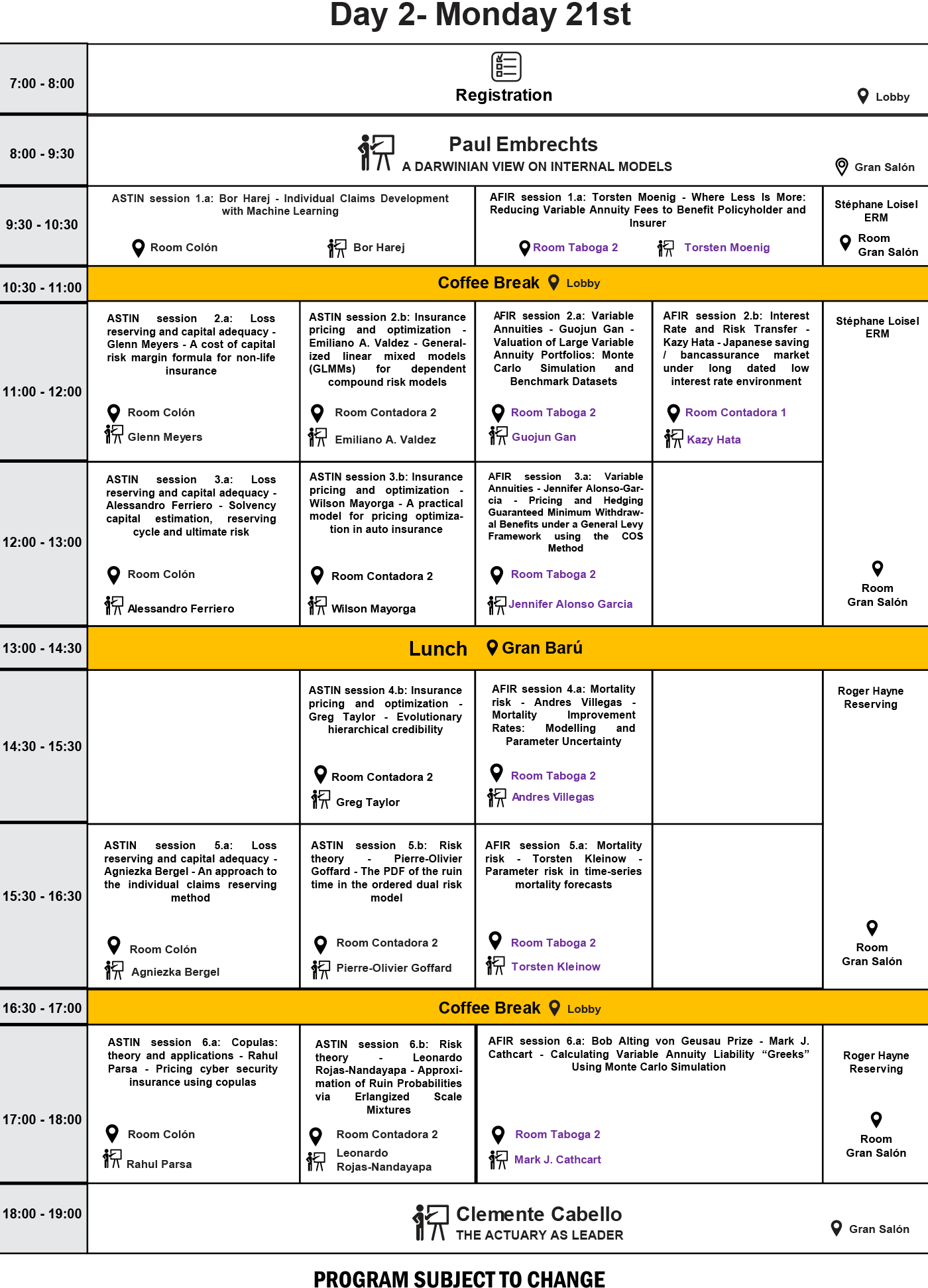

Registration & breakfast

Opening & plenary session

ASTIN parallel sessions

AFIR parallel sessions

Educational Workshop

Lunch

ASTIN parallel sessions

AFIR parallel sessions

Educational Workshop

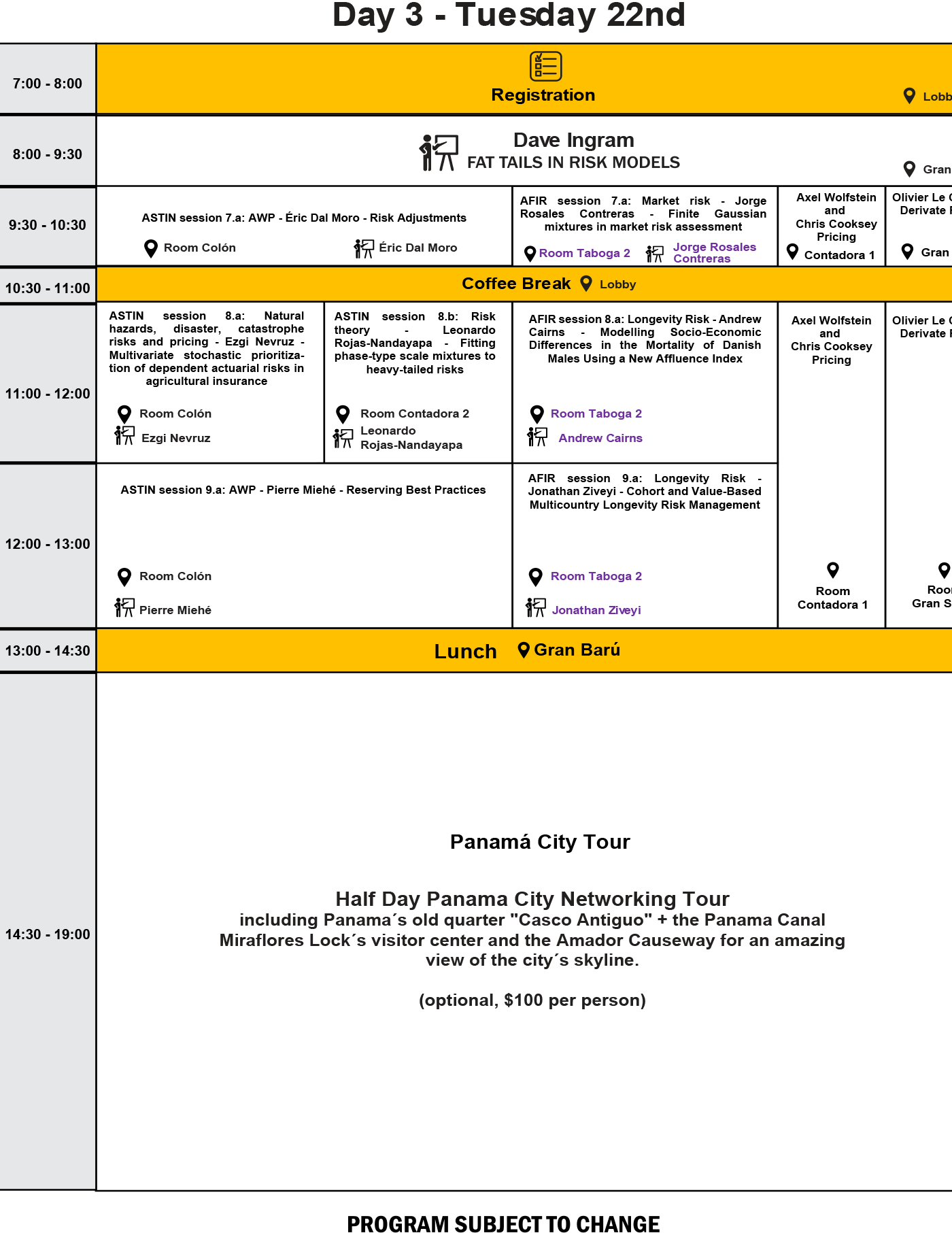

Registration & breakfast

Plenary session

ASTIN parallel sessions

AFIR parallel sessions

Educational Workshop

Lunch

Panama city tour

Registration & breakfast

Plenary session

ASTIN parallel sessions

AFIR parallel sessions

Educational Workshop

Lunch

ASTIN parallel sessions

AFIR parallel sessions

Educational Workshop

ASTIN GA

AFIR GA

Gala Dinner

Registration & breakfast

Plenary session

Educational Workshop

Lunch

Educational Workshop

· Paul Embrechts: “A Darwinian View on Internal Models.”

· Dave Ingram: Fat Tails in Risk Models

· Clemente Cabello: The Actuary as Leader

· Reserving, Roger Hayne

· Enterprise Risk Management, Stephane Loisel

· Pricing, Axel Wolfstein & Chris Cooksey

· Derivative Pricing, Olivier Le Courtois

· Reinsurance, Eberhard Muller & Eric dal Moro

· Bayesian Markov Chain Monte Carlo Models, Glenn Meyers

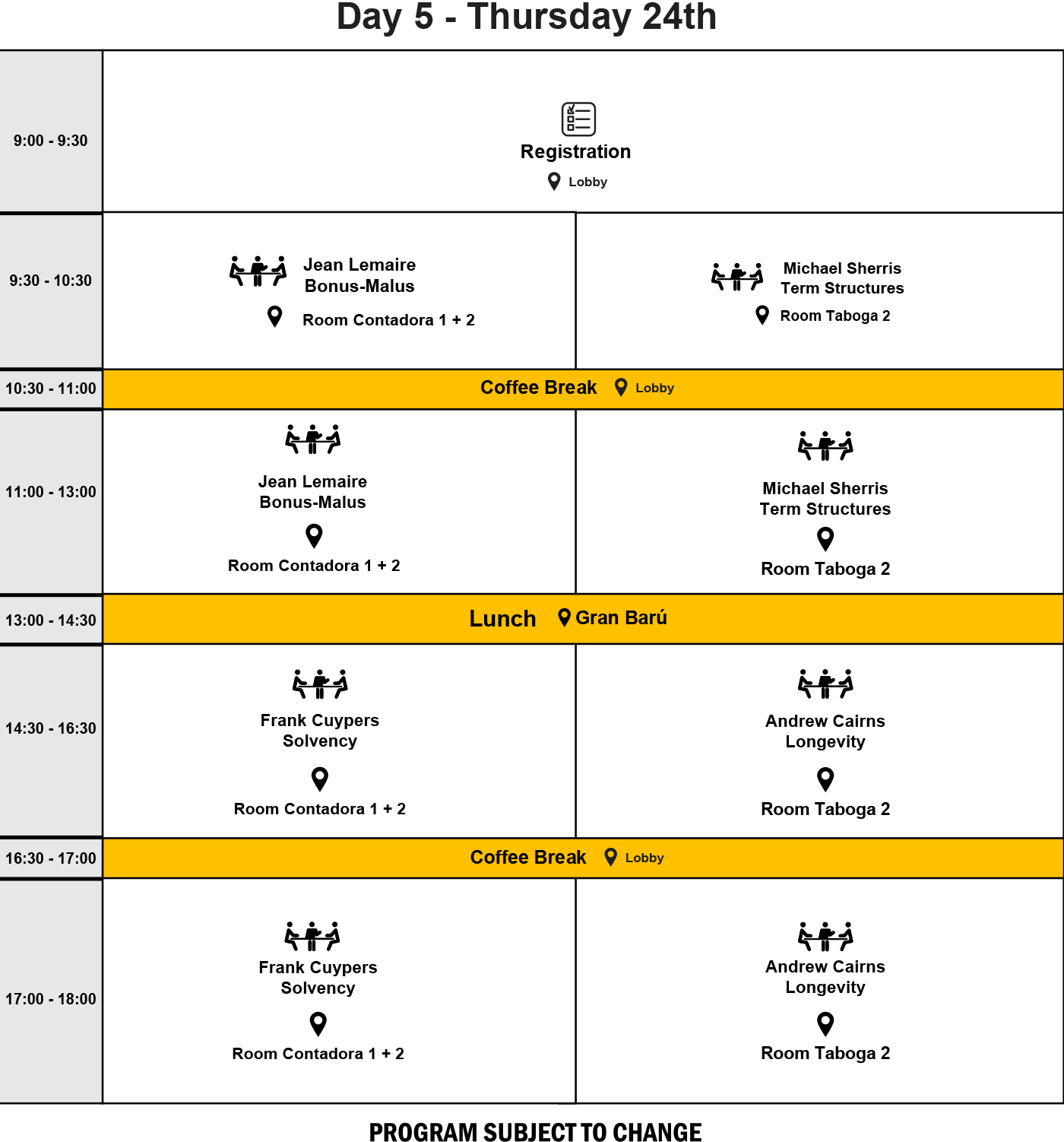

· Bonus Malus Pricing, Jean Lemaire

· Term Structure Models, Michael Sherris

· Solvency, Frank Cuypers

· Longevity, Andrew Cairns

· Loss reserving and capital adequacy

· Insurance pricing and optimization

· Reinsurance and risk transfer

· Risk management

· Natural hazards, disaster, catastrophe risks and pricing

· Capital management, allocation and pricing

· Dividend theory and practice

· Longevity, health, critical illness and employment insurance

· Risk theory

· Copulas: theory and applications

· Extreme value statistics

· Investment and asset allocation

· Portfolio risk management

· Bond portfolio management

· Asset/Liability Management (ALM)

· Enterprise risk management (ERM)

· Risk measures and capital allocation

· Managing retirement accumulations and decumulations

· Dynamic asset allocation

· Asset and derivative pricing

· Longevity, health and mortality risk

· Pricing and risk management for product guarantees

· Solvency and risk based capital